- Trade Treasury Payments | The Liquidity Brief

- Posts

- TTP Liquidity Brief | Issue 51 - A well-fed week at TTP

TTP Liquidity Brief | Issue 51 - A well-fed week at TTP

Breakfast Club, studio sessions, and the latest across trade and payments.

Carter Hoffman

April 27, 2026

🌟 Editor's note

Editor’s Note | Week of 21 April 2026

By Carter Hoffman

TTP’s London team had a busy, but exciting week last week!

We kicked things off with our latest TTP x Sullivan Breakfast Club in London, where over 50 people joined us to talk about fraud in trade finance (we’ve said it before, and we’ll say it again - free coffee and pastries are the best way to lure this industry into a room).

We were also back in TTP Studios this week, recording a new round of interviews and conversations (with some folk that didn’t need pastries to come visit us). Some interviews may have been more serious than others, but we hope that they will all make for some exciting and engaging watching. Keep an eye out over the next few weeks as we get these ready to send your way!

On the editorial side, we’ve been covering a wide range of developments across trade, treasury, and payments. A big theme last week was risk. We looked at how tensions in the Middle East are starting to affect sanctions and AML considerations and how inflation and commodity trends are shaping opportunities in Africa. We also explored changes in payments and treasury, including new thinking on cash management, the impact of payment failures on SMEs, and ongoing work around digital invoicing frameworks.

As always, plenty to read and watch.

Until next time — stay breakfasted.

— The TTP Editorial Team

Week Highlights

TTP x Sullivan Breakfast Club April 2026 - Fraud in trade finance is persistent, predictable, and largely detectable

TTP x Sullivan Breakfast Club April 2026 - UK SME finance is heavily constrained by fraud‑driven risk aversion

TTP x Sullivan Breakfast Club April 2026 - Controls, governance and insurance are now seen as essential risk‑transfer tools

Country of the Week: Mauritius

Did you know that Mauritius was the exclusive home of the famously extinct Dodo bird? It’s true, the large flightless bird known to the scientific community as Raphus cucullatus, lived in the island’s forests which were predator free until the arrival of French and Dutch sailors, who also introduced animals like pigs, dogs, and rats. The last recorded sighting of a dodo took place in 1662.

Mauritius trade stats (2024):

Total exports: $2.49 B | Total Imports: $7 B |

Largest export destination: France ($250 M) | Largest import partner: China ($1.28 B) |

Largest Export: Processed Fish ($284 M) | Largest Import: Refined Petroleum ($1.29 B) |

Source: OEC

Slow Read

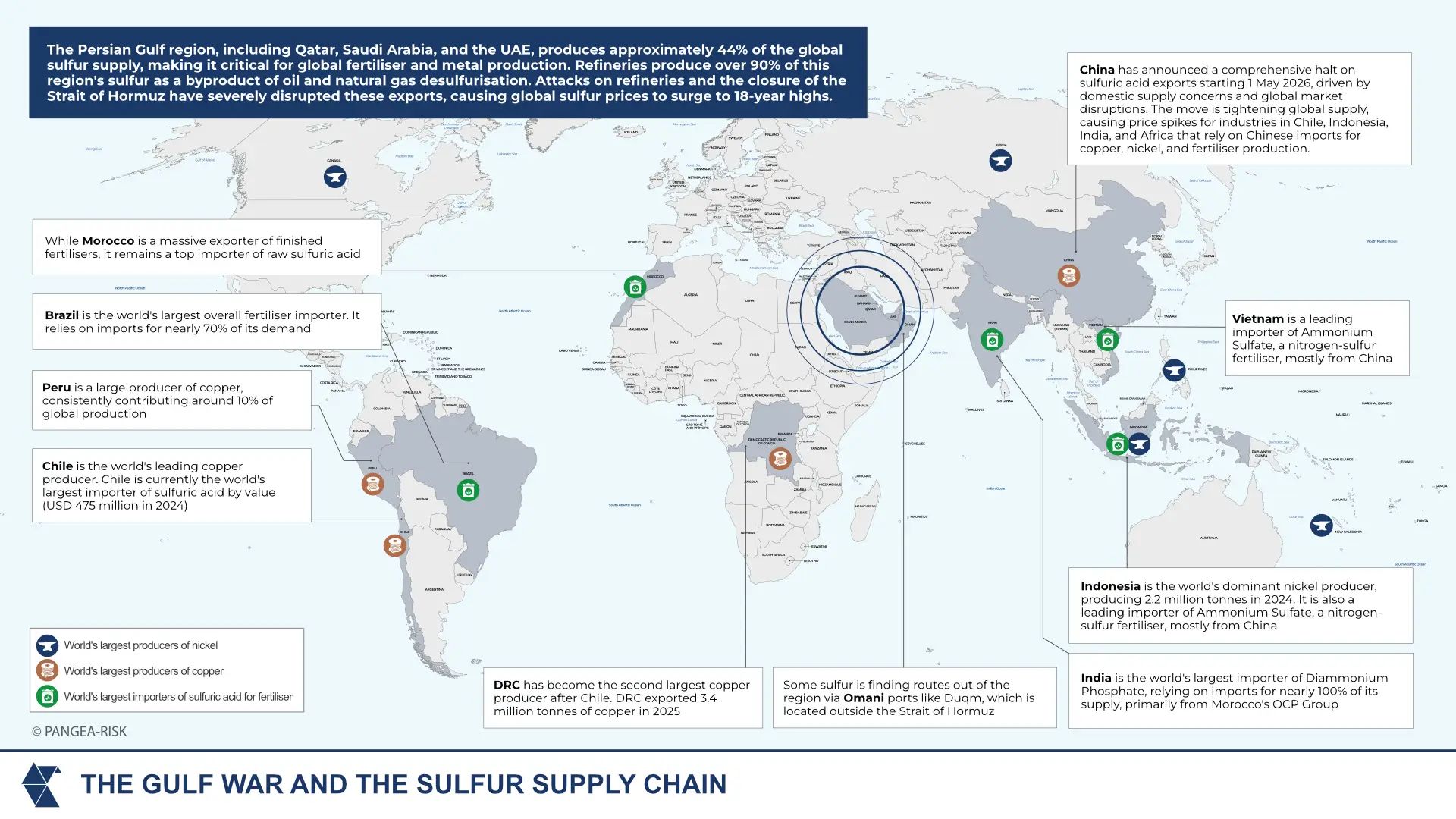

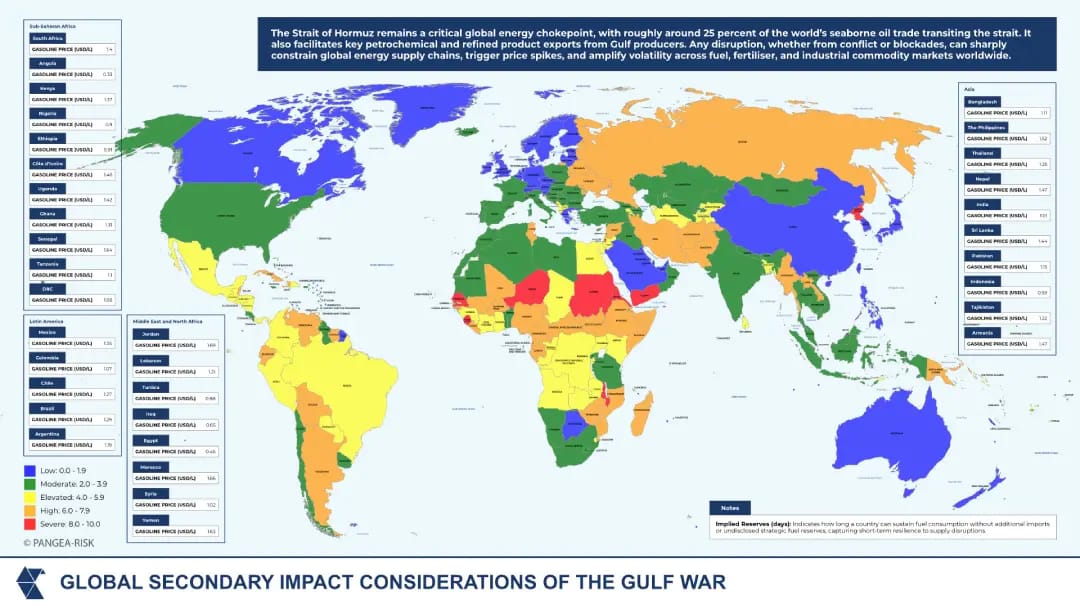

Gulf War: Second-order shocks from Strait of Hormuz disruption reshape global risk dynamics

Prolonged disruption to the Strait of Hormuz is reshaping global energy flows, exposing structural vulnerabilities across import‑dependent economies while testing the limits of geopolitical risk buffers. As shipping constraints, elevated insurance costs, and tighter liquidity conditions persist, second‑order effects are intensifying across the globe. Diverging resilience between commodity exporters and importers is widening macroeconomic imbalances, with rising implications for foreign exchange availability, political stability, and sovereign risk profiles.

On 21 April, the United States (US) announced a unilateral extension of the ceasefire with Iran, even while Iran did not accept the truce and has not committed to reopening the Strait of Hormuz. As the Gulf War, and the associated disruption to the Strait of Hormuz, enter its eighth week, longer‑term impacts are becoming evident. Iran has demonstrated that control over the strait, which carries roughly 20 percent of global oil flows, provides decisive leverage, constraining shipping and destabilising markets. At the same time, the conflict has exposed limits to US security guarantees, particularly in sustaining insurer confidence for vessels transiting the route. Immediate effects include reduced export volumes, rerouted shipping, and elevated freight and insurance costs.

While Gulf producers are mitigating disruptions through alternative pipelines and logistics corridors, these remain insufficient to offset maritime constraints. Energy markets are tightening, delivery timelines are extending, and price volatility is becoming more entrenched. Liquefied Natural Gas (LNG) exports, particularly from Qatar, face logistical bottlenecks, while producers reliant on Hormuz transit are experiencing direct fiscal pressure. The shock is also spreading beyond hydrocarbons. Elevated oil prices are accelerating substitution dynamics in agricultural markets, with rising demand for palm oil and biofuels. Meanwhile, constraints on Gulf sulfur exports, critical for fertiliser and mining, are increasing input costs across agricultural and metals value chains. This is strengthening linkages between energy volatility, food security, and industrial production.

PANGEA‑RISK assesses that the Hormuz disruption now constitutes a structural stress event. Although energy exporters retain sufficient buffers to manage near‑term volatility, import‑dependent economies face rising macroeconomic and political risks driven by higher energy costs, foreign exchange pressure, and tightening financial conditions.

Second-order implications and extended risk transmission

While the immediate disruptions stemming from the Gulf War and the Strait of Hormuz blockade are centred on energy markets and shipping flows, second‑order effects are now materialising across global commodity systems, trade linkages, and geopolitical alignments. These spillovers are reinforcing the assessment that the crisis has evolved into a broader structural shock with multi‑sector implications rather than a contained regional conflict.

A key emerging channel is the reconfiguration of global agricultural and biofuel markets. Elevated crude prices and supply uncertainty are accelerating substitution dynamics, most notably in palm oil. Import‑dependent economies are increasing stockpiling, driving a sharp rise in Southeast Asian exports, particularly from Malaysia and Indonesia. This demand surge is being compounded by increased biofuel utilisation, linking energy market volatility directly to food systems. However, structural constraints, including ageing plantations, climate risks, and rising fertiliser costs, limit supply responsiveness. The result is sustained upward pressure on edible oil prices, amplifying global food inflation and exacerbating vulnerabilities in low‑income, food‑importing economies.

Simultaneously, disruptions to Gulf‑based sulfur production are cascading into global fertiliser and metals value chains. The Persian Gulf accounts for a significant share of global sulfur supply, largely as a byproduct of hydrocarbon refining. Attacks on refining infrastructure and restricted transit through Hormuz have driven sulphur prices to multi‑decade highs. This is feeding into higher input costs for fertiliser production and metal processing, particularly copper and nickel, tightening margins and output across multiple jurisdictions.

These pressures are being intensified by policy responses in key supplier markets. China’s decision to halt sulfuric acid exports from May 2026, driven by domestic supply concerns, is further constraining global availability. This introduces an additional layer of supply risk for major industrial and agricultural economies reliant on imported inputs, including India, Indonesia, Chile, and several African markets. The combined effect of supply disruption and export controls is amplifying price volatility across fertiliser markets, with downstream implications for agricultural productivity and food security.

The transmission of these shocks is particularly pronounced in resource‑dependent and import‑reliant economies. Major copper producers such as Chile, Peru, and the Democratic Republic of Congo (DRC) face rising input costs that could erode export competitiveness, while fertiliser‑importing economies such as Brazil and India are exposed to higher agricultural production costs and inflationary pressures. Morocco, despite its position as a leading fertiliser exporter, remains dependent on imported sulfuric acid, creating a vulnerability within its value chain.

In Southeast Asia, Indonesia’s dual role as a nickel producer and fertiliser importer underscores the complexity of exposure, with industrial output and agricultural inputs simultaneously affected. Logistical adaptations are emerging but remain partial. Oman’s Duqm port is facilitating limited rerouting of sulfur exports outside the Strait of Hormuz, highlighting attempts to mitigate chokepoint risks. However, such alternatives lack the scale to offset systemic disruption, reinforcing the persistence of supply constraints.

Overlaying these economic dynamics is a deteriorating geopolitical backdrop. The fragility of the ceasefire between the US and Iran and uncertainty surrounding negotiations, particularly with no confirmed continuation of talks at the time of writing and escalating rhetoric on both sides, maintain a high risk of renewed confrontation. The continuation of the US blockade and mutual accusations of violations suggest that any resolution remains unlikely in the near term. This sustained uncertainty is entrenching risk premiums across energy, shipping, and insurance markets, while also deterring investment and complicating forward planning for both states and corporates.

In aggregate, these second‑order effects are deepening the asymmetry of global economic impacts. While commodity exporters may benefit from elevated prices in the short term, the broader system is characterised by tighter supply conditions, rising input costs, and increased policy intervention. For structurally weaker economies, particularly those reliant on imported energy, food, and industrial inputs, the convergence of these pressures is likely to accelerate macroeconomic instability, elevate fiscal stress, and heighten socio‑political risk over the medium term.

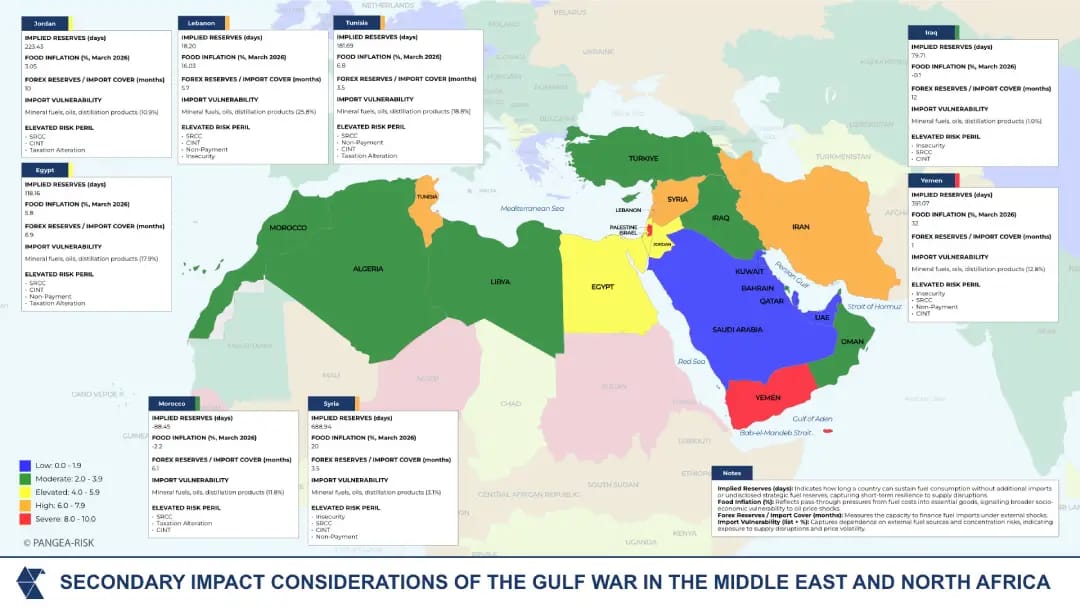

MENA exporters retain buffers, despite import vulnerabilities

Saudi Arabia and the UAE are maintaining export flows through the East‑West pipeline and the Fujairah corridor, but both are operating below capacity as maritime traffic through the Strait of Hormuz remains constrained. Even with these adjustments, cargo delays, elevated insurance costs, and rerouting are reducing realised export volumes and stretching delivery timelines into global markets. Qatar is facing immediate disruption in LNG logistics, with vessel movements restricted and export capacity reduced by around 17 percent, delaying cargo schedules and tightening supply to key buyers. Iraq is already seeing the sharpest impact among producers, with around 90 percent of exports dependent on Hormuz transit, leading to reduced output and delayed revenue inflows. If disruption persists through the next quarter, Iraq will face tighter fiscal liquidity and pressure on budget execution, while Qatar will continue to see constrained LNG delivery even if upstream production remains intact.

The pressure is moving directly into oil‑importing economies through fuel prices, logistics costs, and foreign‑currency availability. Egypt has already raised fuel prices by up to 17 percent, and further adjustments are likely if Brent remains elevated and refined product costs stay tight. This is feeding into electricity tariffs, transport costs, and industrial input prices, while weaker Suez Canal traffic and softer tourism inflows are reducing foreign exchange earnings. Egypt is likely to face continued inflationary pressures and tighter fiscal trade‑offs between subsidy containment and social cost management. Jordan is entering the same cycle, driven by higher import costs and greater service‑sector exposure, with the tourism and transport sectors absorbing the impact of higher shipping and insurance costs. Tunisia and Morocco will face sustained pressure on fuel import bills, with governments likely to expand targeted support for transport and other essential sectors if oil prices remain elevated, thereby increasing fiscal strain and limiting policy flexibility.

Lebanon, Yemen, and Syria are entering a phase where fuel availability becomes the immediate constraint rather than price adjustment. Lebanon’s reliance on imported fuel and limited institutional capacity means that rising costs are already feeding into electricity generation and household expenditure, with further deterioration likely if supply chains remain disrupted. Yemen is facing a simultaneous tightening of fuel and food supplies, as maritime constraints and port bottlenecks reduce import volumes, increasing the risk of shortages in key urban centres. Syria is likely to experience further reductions in fuel availability as external supply becomes harder to secure, feeding into transport, agriculture, and local distribution networks.

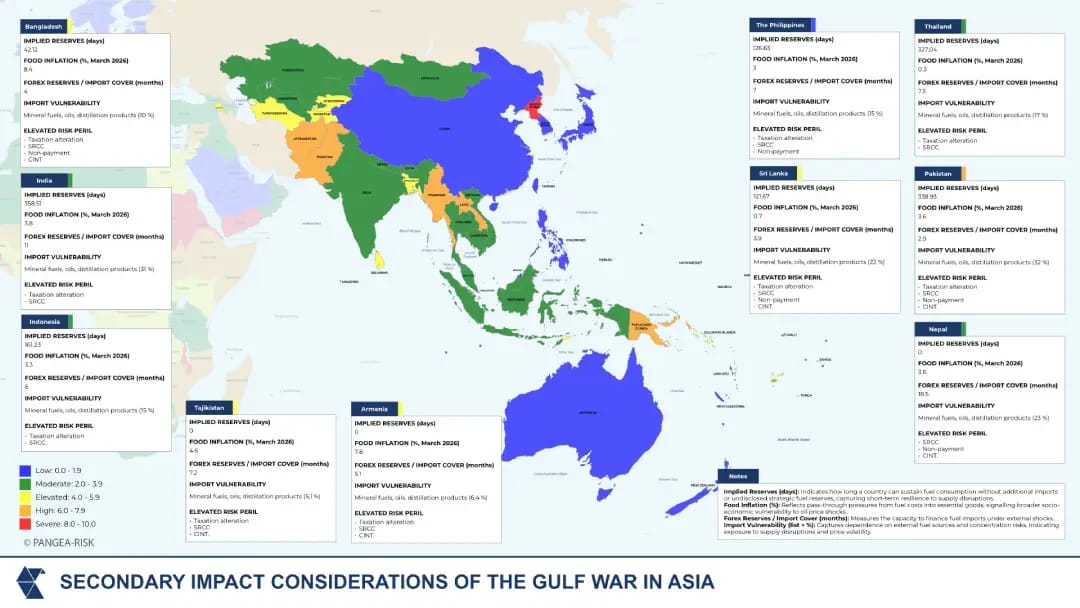

Uneven buffers and energy risks across Asia

The Gulf War is transmitted into Asian importers through higher crude and refined fuel prices, rising freight and insurance costs on westbound trade routes, and tighter pressure on external balances. The effect is strongest in economies that combine high fuel import dependence with shallow buffers, notably Bangladesh, Pakistan, Sri Lanka, and Nepal. In these markets, higher import costs are likely to pass quickly into transport, electricity, and food prices, raising the risk that inflation becomes broader and more politically sensitive. The shock is therefore not confined to energy markets. It is also increasing fiscal strain, complicating exchange‑rate management, and narrowing room for monetary easing across several economies already facing fragile social conditions. Several Asian countries face prospects of reduced remittances from migrant workers if there is a protracted slowdown in Gulf economies.

The regional picture nonetheless diverges sharply. India is better placed to absorb a prolonged disruption because of stronger import cover, larger foreign exchange reserves, and substantial domestic refining capacity, although its large import dependence still means that sustained high oil prices would complicate inflation management and increase pressure on subsidy and tax decisions. Indonesia and Thailand also retain greater macroeconomic flexibility, but both remain exposed to imported energy costs feeding into consumer prices and industrial input costs. By contrast, Pakistan and Sri Lanka face a more acute external account risk if Gulf disruption persists, as relatively thin import cover leaves less room to smooth higher fuel bills without renewed pressure on currencies, financing needs, and public finances.

Smaller frontier markets such as Nepal and Tajikistan are likely to feel the shock disproportionately despite their lower absolute demand, because high dependence on imported fuel, limited market depth, and weaker shock absorption capacity magnify pass‑through effects. Governments will increasingly have to choose between allowing higher retail prices, which raises the probability of strikes and broader unrest, or containing prices through subsidies and tax adjustments, which worsens fiscal and external pressures. Over time, should disruption in the Gulf persist, the principal fault line across Asia will shift away from a simple distinction between energy importers and non‑importers, towards a more consequential divide between states capable of absorbing a sustained energy shock and those for which such pressures rapidly translate into broader macroeconomic and political instability.

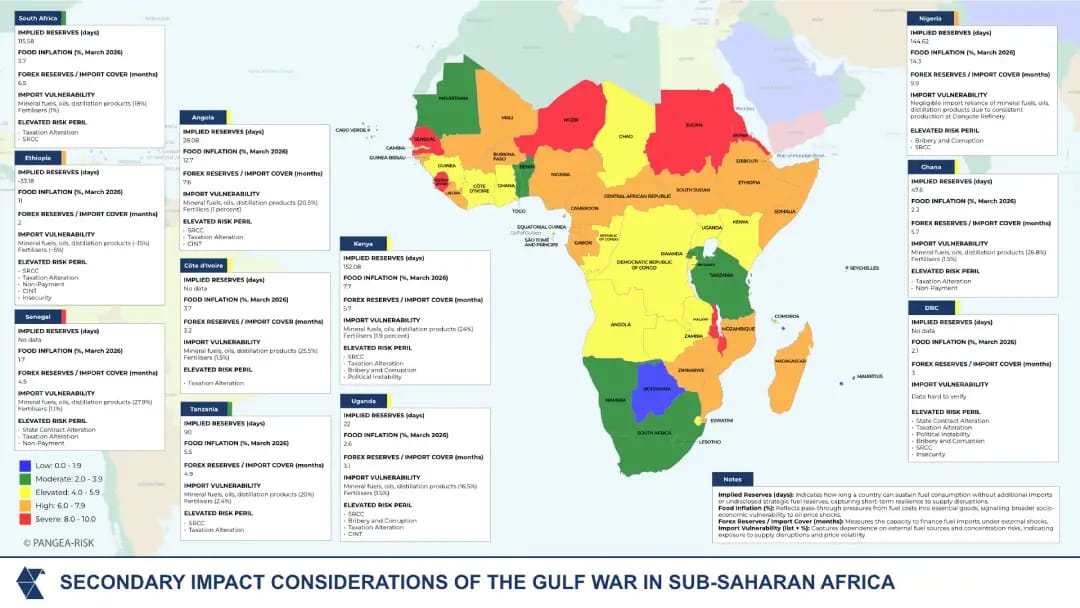

Economic contractions exert pressure on Africa

For Sub‑Saharan African countries, the ongoing war and disruption to transit through the Strait of Hormuz have reversed the broad‑based positive growth outlooks anticipated at the start of the year. Following its 2026 Spring Meetings, the IMF revised its regional growth forecast from 4.5 to 4.3 percent, cautioning that elevated import costs will erode “hard‑fought” macroeconomic gains observed in 2025. Critically, elevated prices for food, fuel, and fertilisers, alongside renewed currency and inflationary pressures, are set to constrain fiscal space, amplifying vulnerabilities in lower‑income and import‑dependent markets.

Nigeria is a notable exception in this environment, benefiting from strong refining facilities and the prospect of higher crude export receipts. The 2026 budget benchmarked prices of crude at USD 64.9 per barrel, while futures reached as high as USD 111 per barrel in March. Data from the Central Bank of Nigeria (CBN) shows that the country exported 55.39 million barrels over the first two months of the year, prompting President Bola Tinubu to increase the national budget to a record NGN 68.32 trillion (approximately USD 49.3 billion). Consistent production at the Dangote Refinery has also eliminated the need for imported refined petroleum products, which cost the government USD 11.5 billion in 2024. On 17 April, the Dangote Group announced its first oil extraction from OML 71 and OML 72 in the Niger Delta, signifying progress towards full domestic supply chain integration. Such advancement further reduces the reliance on crude deliveries from the Nigerian National Petroleum Company (NNPC), bridging a supply shortfall seen at the start of the year.

Across the rest of the continent, the outlook is less favourable. South Africa is the continent’s largest importer of refined petroleum, with a major decline in domestic refining output over the past decade. In Kenya, recent irregularities in fuel procurement and rising pump prices have heightened the risks of strikes, riots, and civil unrest in the coming weeks. Deep‑rooted grievances stemming from the 2025 Gen‑Z protests remain unresolved, and there is a severe threat of renewed commercial shutdown in urban centres if lawmakers do not make further concessions to shield consumers from soaring costs. Fuel shortages and long queues at filling stations in Malawi and the DRC underscore a broader continental dependency on compromised global supply chains, with an estimated 70 percent of consumed petrol products on the continent imported.

While the International Energy Agency (IEA) mandates that member countries maintain reserves of 90 days, strategic buffers across African countries are far below this threshold and poorly documented. Such uncertainty heightens social anxiety and undermines investor confidence, notably when government statements contradict the observed reality on the ground. Looking ahead, further shortages are likely as shipping disruption persists into its ninth week.

Energy windfalls and inflation in Latin America

The Gulf War’s impact on Latin America is transmitted primarily through higher commodity and oil prices, and tighter macro‑financial conditions. The increase in oil prices is improving the terms of trade for major producers such as Brazil and Colombia, strengthening external balances, supporting currencies, and easing fiscal pressures in countries with weaker public finances. This has reinforced the region’s role as a strategic alternative supplier of hydrocarbons, drawing renewed investor interest into oil and LNG projects, particularly in Brazil and Argentina. Over time, this is likely to deepen capital allocation toward extractive sectors, even as it raises questions about longer‑term diversification and exposure to commodity cycles.

At the same time, the inflationary effects of higher energy and input costs are complicating macroeconomic management. Even in oil‑exporting economies, the pass‑through from refined fuel imports is significant, feeding into transport and food prices. In Brazil, where monetary easing had been expected, the rise in inflation linked to higher oil prices is already narrowing the scope for interest rate cuts and pushing the central bank toward a more cautious stance. This dynamic is visible across the region, where sustained energy price pressure risks adding over one percentage point to inflation, with particularly strong effects in more import‑dependent economies.

Country outcomes diverge accordingly. Brazil and Colombia are set to benefit from improved external positions but face tighter monetary trade‑offs. Argentina will see stronger incentives to expand shale and LNG capacity, although financing constraints persist. Mexico is balancing emerging opportunities in LNG re‑exports with the fiscal cost of shielding consumers from higher fuel prices. Chile remains the most exposed, with rising energy import costs feeding directly into inflation and external vulnerabilities. These pressures are feeding into domestic political risk, as governments weigh subsidy regimes against fiscal discipline, while higher living costs increase the likelihood of social tensions and policy volatility.

Insight

The Gulf War’s disruption to energy and commodity markets is now translating into a broader escalation of country risk perils across the Middle East and North Africa (MENA), Asia, Sub‑Saharan Africa (SSA), and even Latin America, increasingly exposed through second‑order transmission channels.

Rising fuel and input costs are intensifying Political Instability and Strikes, Riots and Civil Commotion (SRCC) risks, particularly in import‑dependent economies where inflation is feeding into transport, electricity, and food prices. Governments are responding through subsidies, price controls, and ad hoc interventions, heightening risks of Taxation Alteration, State Contract Alteration, and in more extreme scenarios, potentially Confiscation, Expropriation, Nationalisation, and Deprivation (CEND)‑related actions in strategic sectors such as energy and mining. Tighter fiscal space and external balances are also increasing Currency Inconvertibility and Non‑Transfer (CINT) risks, especially in frontier and lower‑reserve economies in Asia and Africa, where higher import bills are accelerating foreign exchange depletion. This is compounding Non‑Payment risk, as sovereigns and state‑owned entities face rising debt servicing pressures alongside declining revenue predictability.

At the same time, disruptions to fertiliser and metals supply chains, exacerbated by potential export controls, are raising production costs and weakening industrial output. This is prompting greater policy intervention, increasing regulatory and compliance burdens as firms navigate constrained supply chain environments. Across regions, the cumulative effect is a shift from cyclical volatility to structural risk deterioration. While commodity exporters in Latin America and parts of SSA benefit from price upside, the broader environment is characterised by rising interventionism, reduced policy predictability, and heightened socio‑political fragility, dynamics that will increasingly define the country risk landscape if disruption persists.

Trade digest

Treasury, payment and global banking digest

🗓️ Upcoming events

2026 BAFT Global Annual Meeting

| The 2026 Payments Canada SUMMIT

|

Commodity Trading Week Europe

| TXF Amsterdam 2026 - Global Natural Resources and Commodities Finance

|

ITFA Americas 29th Annual Conference, Miami

| ICISA 100th Anniversary

|

Money 2020

| EBRD 2026 Annual Meeting and Business Forum

|

FCI 58th Annual Meeting

| ICC Austria's Trade Finance Week 2026

|